When debt becomes overwhelming, the instinct is to find help quickly. A search online brings up dozens of companies promising relief, lower payments, or negotiated settlements. The challenge is not finding options. It is figuring out how to compare them intelligently.

Many consumers begin by searching for the best debt settlement companies, but the real value lies in understanding how to evaluate providers rather than chasing rankings. Lists and advertisements can only tell part of the story. Choosing the right financial assistance provider requires asking the right questions and understanding what truly matters.

Instead of focusing on flashy claims or bold guarantees, it helps to approach the comparison process like a checklist. What are you actually buying, and how do you know it is credible?

Start with Your Own Financial Snapshot

Before comparing providers, clarify your own situation. How much debt do you have? What types of accounts are involved? Are you current on payments, or already behind?

Different providers specialize in different approaches. Some focus on debt management plans through nonprofit counseling. Others negotiate settlements with creditors. Some assist with consolidation or structured repayment programs.

The Consumer Financial Protection Bureau provides clear explanations of various debt relief options. Reviewing these basics helps you understand what type of service might fit your needs before contacting companies.

Comparing providers without knowing your own financial details is like shopping for insurance without knowing what coverage you need.

Examine Transparency Around Fees

One of the most important comparison points is fee structure. Legitimate financial assistance providers should clearly explain how and when they charge fees. Are fees based on a percentage of enrolled debt? Are they contingent on successful settlements? Are there setup or monthly administrative fees? Everything should be in writing. Be cautious of companies that require large upfront payments before services begin. The Federal Trade Commission warns consumers about advance fee debt relief schemes.

When comparing providers, place transparency at the top of your criteria list. If fee explanations are vague or overly complicated, that is a sign to slow down.

Understand the Process and Timeline

No legitimate provider can eliminate debt instantly. Any reputable company should be able to explain the process step by step.

Ask how long the program typically lasts. Ask what happens if a creditor refuses to negotiate. Ask how missed payments or unexpected financial changes are handled.

Comparing providers becomes easier when you map out their processes side by side. One may emphasize structured payment plans. Another may focus on negotiated reductions. The best fit depends on your income stability and risk tolerance.

A provider that promises guaranteed results without explaining the steps in detail is not offering a realistic solution.

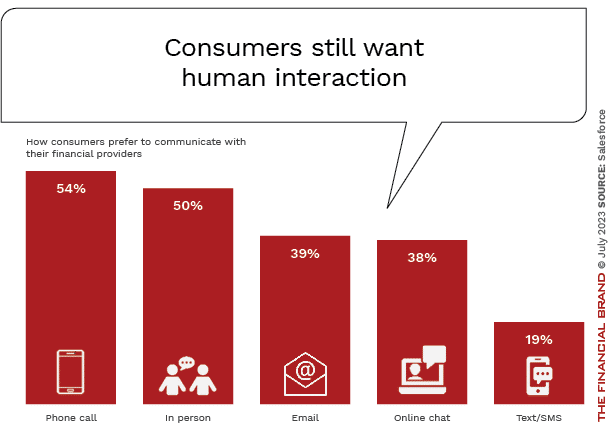

Look at Communication and Accessibility

Financial assistance programs can last months or even years. During that time, communication matters.

How easy is it to reach a representative? Is there a dedicated advisor, or do you speak with different people each time? Are updates provided regularly?

During initial consultations, pay attention to how clearly questions are answered. If representatives are patient, transparent, and willing to explain details, that is a positive sign. If they rush conversations or pressure you to sign immediately, that is a concern.

You are not just comparing programs. You are evaluating long term working relationships.

Review Credentials and Compliance

Another important comparison point is regulatory compliance. Check whether the company operates legally in your state and whether it has a history of complaints.

You can research consumer complaints through the Consumer Financial Protection Bureau complaint database. While no company is immune to occasional negative feedback, patterns of unresolved complaints are worth noting.

Also look for accreditation or memberships in recognized industry organizations. Although accreditation alone does not guarantee quality, it can indicate adherence to certain standards.

Due diligence protects you from choosing based solely on marketing.

Consider Impact on Credit and Taxes

Different financial assistance options affect credit differently. Debt management plans may have less severe credit impact than settlement programs that involve stopping payments before negotiation.

Additionally, forgiven debt in settlement scenarios may have tax implications. Any reputable provider should explain these potential consequences clearly.

When comparing providers, ask direct questions about how their approach may influence your credit score and tax responsibilities. If a company dismisses these concerns or minimizes potential downsides, that is a red flag.

A balanced explanation that includes both benefits and risks signals credibility.

Evaluate Educational Support

Strong financial assistance providers do more than negotiate balances. They often provide budgeting tools, financial education, and long term planning support.

Ask whether the program includes counseling on spending habits, emergency savings, or rebuilding credit. Sustainable financial recovery requires more than resolving current balances.

A provider focused solely on quick settlements without discussing long term stability may not support lasting improvement.

Avoid Pressure and Guarantees

Finally, pay attention to tone. Providers that push urgency or promise guaranteed outcomes should be approached cautiously.

Debt resolution involves negotiation and creditor participation. No company can guarantee specific reductions or timelines in every case.

Take time to compare options calmly. Review written materials carefully. Discuss the decision with trusted family members or advisors if needed.

Choosing a financial assistance provider is a significant decision. It should not feel rushed or confusing.

Making an Informed Decision

Comparing financial assistance providers is less about finding the flashiest promise and more about identifying transparency, credibility, and alignment with your personal situation.

Start with your own financial facts. Examine fees and processes carefully. Verify credentials. Ask about credit impact. Evaluate communication style.

By approaching the comparison process methodically, consumers move from reacting to stress toward making informed choices. Financial assistance should reduce uncertainty, not add to it.

When you focus on clear criteria rather than marketing claims, you are far more likely to select a provider that genuinely supports your path toward financial stability.